Example -4

A piece of construction equipment has initial cost and estimated salvage value of Rs.1500000 and Rs.200000 respectively. The useful life of equipment is 10 years. Find out the year in which the switching from double-declining balance method to straight-line method takes place.

Solution:

Initial cost of the asset = P = Rs.1500000, Salvage value = SV = Rs.200000

Useful life = n = 10 years

The constant annual depreciation rate ‘dm' for double-declining balance (DDB) method is calculated as follows;

![]()

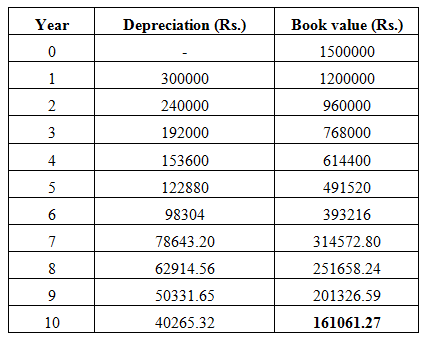

The annual depreciation amount and the book value at the end different years using DDB method are presented in Table 3.5.

Table 3.5 Depreciation and book value using double-declining balance method

From the above table it is noted that the book value at the end of useful life i.e. 10th year is Rs.161061.27, which is less than the estimated salvage value i.e. Rs.200000. Thus the total depreciation amount over the useful life is more than the desired. Hence switching from double-declining balance method to straight-line method is carried out and is presented in Table 3.6.

In Table 3.6, annual depreciation by SL method, selected depreciation amount and book values are calculated in the same manner as that in the previous example. The annual depreciation for 10th year in DDB method is Rs.40265.32 and subtracting this amount from 9th year book value results in a book value (at the end of 10th year) less than the estimated salvage value (As seen from Table 3.5). Further the book value at the end of 9 th year (i.e. Rs.201326.59) is greater than salvage value. Thus switching from DDB method to SL method takes place in 10th year. With switching from DDB method to SL method, the book value at the end of 10 years is equal to Rs.200000 (same as the estimated salvage value) as compared to Rs.161061.27 without switching to straight-line method.