Switching between different depreciation methods:

Switching is carried out from one depreciation method to another to accelerate the depreciation of book value of the asset and thus to have income tax benefits. Switching takes place when depreciation amount of an asset for a given year in the present depreciation method is less than that in the new depreciation method. The most commonly used switching is from double-declining balance (DDB) method to straight-line (SL) method. In double-declining balance method, the book value as calculated by using equation (3.17) never reaches zero. In addition the calculated book value at the end of useful life does not match with the salvage value. Switching from double-declining balance method to straight-line method ensures that the book value does not fall below the estimated salvage value of the asset.

In the following examples the procedure of switching from double-declining balance method to straight-line method is illustrated.

Example -3

The initial cost of an asset is Rs.1000000. It has useful life of 9 years. The estimated salvage value of the asset at the end of useful life is zero. Calculate the annual depreciation and book value using double-declining balance method and find out the year in which the switching is done from double-declining balance method to straight-line method.

Solution:

Initial cost of the asset = P = Rs.1000000

Useful life = n = 9 years

Salvage value = SV = 0

For double-declining balance (DDB) method, the constant annual depreciation rate ‘dm' is given by;

![]()

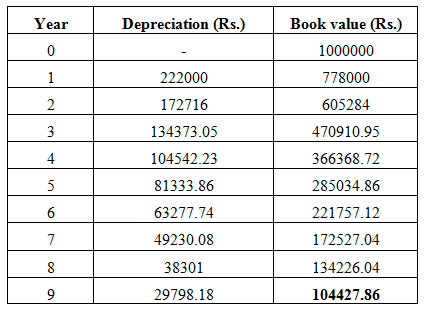

The annual depreciation and the book value at the end different years are calculated using the respective equations stated earlier and are presented in Table 3.3.

Table 3.3 Depreciation and book value from double-declining balance method

From the above table it is observed that the book value at the end of useful life is Rs.104427.86, which is more than the estimated salvage value i.e. 0. The asset is not completely depreciated. Thus switching is carried out from double-declining balance method to straight-line method and is shown in Table 3.4.