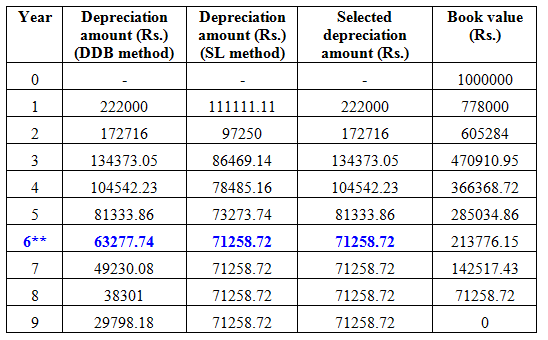

Table 3.4 Double-declining balance method and switching to straight-line method

** Switching from DDB method to SL method

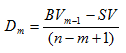

In the above table, annual depreciation values from double-declining balance (DDB) method are also presented to compare with those obtained from straight- line method. For straight-line (SL) method the depreciation amount for a given year ‘m ' is calculated by dividing the difference of the book value (at the beginning of that year) and salvage value by the number of years remaining from beginning of that year till the end of useful life and is shown below;

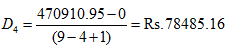

For illustration, the straight-line depreciation in 4th year ( m = 4) is calculated as follows;

From the annual depreciation values by straight-line method as shown in 3rd column of above table, it is observed that, the annual values are not uniform. This is because when switching is carried out from DDB method to SL method, the larger depreciation amount between the two the methods for a given year is subtracted from the previous year's book value to calculate the book value at the end of desired year and this book value is used for calculating the depreciation amount for next year in straight-line method. The larger annual depreciation values (i.e. selected depreciation amount) between DDB method and SL method are provided in 4th column of Table 3.4. The book value at the end of a given year presented in 5th column of above table is obtained by subtracting ‘selected depreciation amount' of that year from the previous year's book value. From Table 3.4, it is observed that the annual depreciation amount in DDB method is greater than that in SL method from 1st year to 5th year and from 6th year onwards the annual depreciation is greater in SL method than that in DDB method. Thus switching from DDB method to SL method takes place in 6th year. With switchover from DDB method to SL method the book value at the end of useful life i.e. 9th year is equal to zero (same as the estimated salvage value) as compared to Rs.104427.86 without switching to straight-line method. In addition the total depreciation amount over the useful life of the asset (initial cost minus salvage value) with switchover from DDB method to SL method is Rs.1000000 (i.e. sum of values in 4th column of Table 3.4) as desired whereas the total depreciation amount without switchover is Rs.895572.14 (sum of values in 2nd column of Table 3.4).