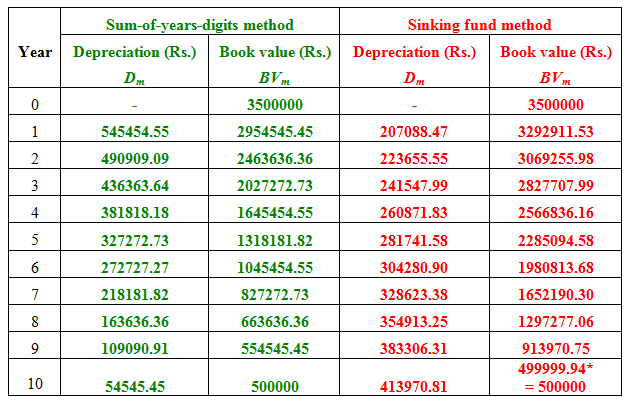

Similarly the annual depreciation and book value at the end of other years are calculated in the same manner and are given in Table 3.2.

The book value at the end of a given year can also be calculated by using equation (3.48). Using this equation, the book value at the end of 2nd year is given by;

Table 3.2 Depreciation and book value of the construction equipment using sum-of-years-digits method and sinking fund method

* This minor difference is due to effect of decimal points in the calculation.

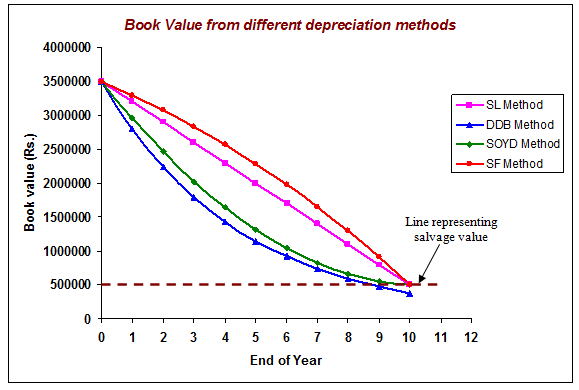

The book value at the end of all years over the useful life of the construction equipment obtained from different depreciation methods (Example 1 and Example 2) are shown in Fig. 3.1.

Fig. 3.1 Book value of the construction equipment using different depreciation methods

In the above figure, the line representing the salvage value is also shown. In double-declining balance method only, the calculated book value at the end of useful life i.e. 10th year is not same as the estimated salvage value.