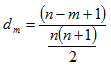

The depreciation rate ‘dm' for any year ‘m' is given by;

(3.21) |

Where n = useful life of the asset as stated earlier

SOY = sum of years' digits over the useful life = ![]()

Rewriting equation (3.21);

|

(3.22) |

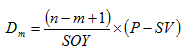

The depreciation amount in any year is calculated by multiplying the depreciation rate for that year with the total depreciation amount (i.e. difference between initial cost ‘P' and salvage value ‘SV ') over the useful life.

Thus the expression for depreciation amount in any year ‘m ' is represented by;

(3.23) |

Putting the value of ‘dm' from equation (3.21) in equation (3.23) results in the following;

|

(3.24) |

The depreciation in 1st year i.e. ‘D1' is obtained by putting ‘m ' equal to ‘1' in equation (3.24) and is given by;

|

(3.25) |

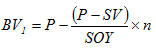

The book value at the end of 1st year is equal to initial cost less the depreciation in the 1st year and is given by;

![]()

Now putting the expression of ‘D1' from equation (3.25) in the above expression results in following;

|

(3.26) |

The depreciation in 2nd year i.e. ‘D2' is given by;

(3.27) |

Book value at the end of 2nd year is equal to book value at the beginning of 2nd year (i.e. book value at the end of 1st year) less the depreciation in 2nd year and is given by;

![]()