The difference between equivalent worth methods (present worth method/future worth method/annual worth method) and rate of return method is that; in case of former, the equivalent worth of the cash inflows and cash outflows are determined at MARR whereas in case of latter, a rate is determined which equates the equivalent worth of cash inflows to that of the cash outflows and the resulting rate is compared against MARR. The rate of return and MARR are expressed in terms of percentage per period i.e. mostly percentage per year.

In the following example, the illustration of the procedure for determination of rate of return for an alternative is presented.

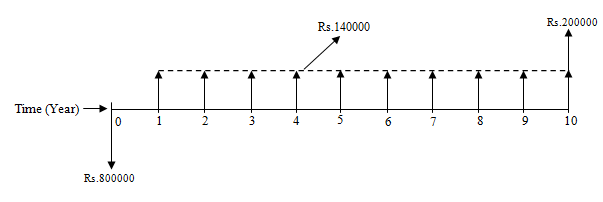

Example -14

A construction firm is planning to invest Rs.800000 for the purchase of a construction equipment which will generate a net profit of Rs.140000 per year after deducting the annual operating and maintenance cost. The useful life of the equipment is 10 years and the expected salvage value of the equipment at the end of 10 years is Rs.200000. Compute the rate of return using trial and error method based on present worth, if the construction firm's minimum attractive rate of return (MARR) is 10% per year.

Solution:

The cash flow diagram of the construction equipment is shown in Fig. 2.29.

Fig. 2.29 Cash flow diagram of the construction equipment

For determination of rate of return ‘ir’ of the construction equipment, first the equation for net present worth of cash inflows and cash outflows is equated to zero. Then using the trial and error method the value of ‘ir’ is determined. The net present worth of cash inflows and cash outflows of the construction equipment is given by the following expression.

![]()

For determining the value of ‘ir’ the net present worth is equated to zero.

![]()