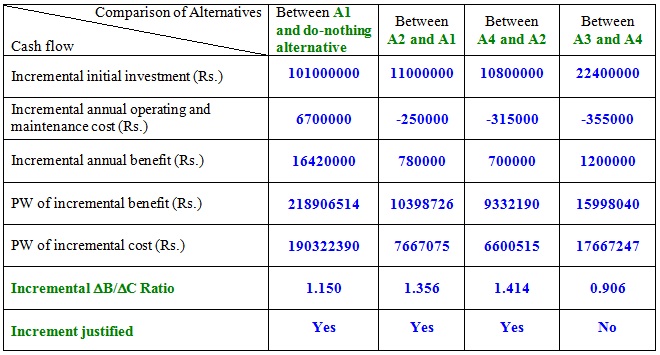

The lowest equivalent cost alternative A1 is first compared against do-nothing alternative i.e. the B/C ratio of alternative A1 on its cash flow is calculated.

B/C ratio of alternative A1 = 1.150

As the B/C ratio of alternative A1 is greater than 1.0, A1 now becomes the base alternative and is compared against the next higher equivalent cost alternative i.e. alternative A2. Now the incremental benefits and incremental costs between A2 and A1 are calculated and the incremental B/C ratio is obtained.

Incremental annual benefits (between A2 and A1) = 17200000 - 16420000 = 780000

Present worth (PW) of incremental annual benefits = 780000(P/A, 7%, 40)

= 780000 X 13.3317 = 10398726

PW of incremental benefits (between A2 and A1) = Rs.10398726

Incremental annual benefits (between A2 and A1) = 112000000 - 101000000 = 11000000

Incremental annual operating and maintenance cost (between A2 and A1) = 6450000 - 6700000

= -250000

Present worth (PW) of incremental annual benefits = 11000000 - 250000(P/A, 7%, 40)

= 11000000 - 250000 X 13.3317 = 7667075

PW of incremental costs (between A2 and A1) = Rs.7667075

![]()

Incremental B/C ratio (between alternative A2 and A1) = 1.356

The incremental B/C ratio between alternatives A2 and A1 can also be calculated by finding out the ratio of the differences in present worth of benefits of alternatives to that of costs. This calculation is shown below.

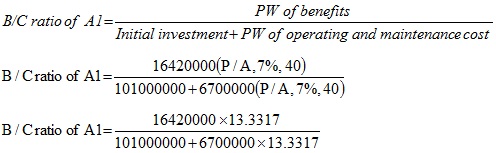

PW of benefits of alternative A1 = 16420000(P/A, 7%, 40)

= 16420000 X 13.3317 = 218906514

PW of costs of alternative A1 = 101000000 + 6700000(P/A, 7%, 40)

= 101000000 + 6700000 X 13.3317 = 190322390

PW of benefits of alternative A2 = 17200000(P/A, 7%, 40)

= 17200000 X 13.3317 = 229305240

PW of costs of alternative A2 = 112000000 + 6450000(P/A, 7%, 40)

= 12000000 + 6450000 X 13.3317 = 197989465

Thus same incremental B/C ratio is obtained.

As the incremental B/C ratio is greater than 1.0, alternative A2 becomes the new base alternative and alternative A1 is removed from further analysis. Alternative A2 is now compared against the next higher equivalent cost alternative i.e. alternative A4. The incremental B/C ratio between alternatives A4 and A2 is determined in the same manner as that was determined between alternatives A2 and A1.

Now the entire calculation for selecting the best alternative using incremental B/C ratio analysis is presented in Table 2.8.

Table 2.8 Comparison of alternatives using incremental B/C ratio* analysis

* Conventional B/C ratio