FINANCIAL EVALUATION – EQUITY INVESTOR'S PERSPECTIVE

Investors' decision to invest in a project depends on the expected returns from the project. Investors usually have a hurdle rate for the return above which an investment is acceptable, and below which the investment is not attractive to them. The hurdle rate normally depends on the cost of capital to the investors and the additional return over cost of capital required for particular types of risk they will be bearing if they participate in the project. The level of risk exposure to the equity investors changes based on the timing of equity commitment, i.e. particular phase in which investors make the equity investment. It is normally considered that the development phase is highly risky while the operation phase to be low risk and construction phase is treated to be medium risk. If a new equity investors participate in the project in later stages of project lifecycle such as after the construction phase, the equity IRR required by the new investors will be lower the return earned by the project sponsor who have developed the project. The required return on equity investment therefore declines as it passes through the various stages of project lifecycle. Equity IRR for projects with moderate risk such as power project with off-take contract or infrastructure with limited demand risk, tend to be in the range of 12-20%.

Equity investments to an infrastructure project are normally provided by two categories of investors, passive investors and active investors. The priority of payments to passive investors is senior to active investor and junior to lenders. Passive investors will get their return from the cash flow that is left after meeting the debt service obligations. As a result, the active investor's rate of return on equity exceeds the passive investor's rate of return as the active investors have greater risk exposure.

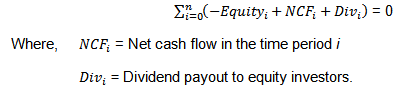

In addition to meeting the hurdle rate, equity investors also require the investment to show positive NPV and to achieve a minimum payback period. Payback period is the time required to recover the original investment through annual cash flows. Investors normally require a maximum payback period of not more than a certain number of years. Investors prefer shorter payback period as it correspond to a high average annual net cash flow. Payback period for equity investors is the point in time when equity investment is covered by the benefits generated during the operation phase, which could be calculated as follows:

Dividend payout to the equity investors is added back to the net cash flow available as the project is credited with generated these benefits. The payback period can be determined by determining the value of time period when the cumulative cash flows equal or exceed the equity investment.