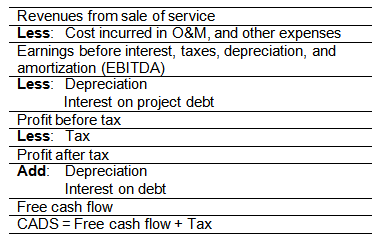

CADS is an important variable in financial evaluation of project company and it is the starting point for any lender to assess how much it may lend to a project company. The typical format for estimating the CADS in a particular year of project operation is given below:

PLCR indicates the project company's capacity overall long term capacity to cover the project debt as a total capital amount. It does not take into account how the cash flows may occur during the project's life. The loan is considered to be less risky, larger the ratio. PLCR helps lender to check whether the project has enough capacity to make service its debt obligations after the term of the loan, in case there have been difficulties in repaying all of the debt in time.

Loan life coverage ratio (LLCR) is similar to project loan life coverage ratio. However, LLCR concentrates on assessing the project company's ability to cover project debt over the term of the loan only and not over the entire project duration.

LLCR = PV (CADS during loan life)/PV (Total Debt)

LLCR is a useful measure for measurement for the initial assessment of the project's ability to service its debt as a whole, but it is not useful if there are likely to be significant cash flow fluctuation from one time period to another.

Annual debt service coverage ratio (ADSCR) can be defined as the ratio of cash generated to debt service in any time period. This is used to assess the project company's ability to service its debt from its annual cash flow. It also given an indication on the amount of risk in the project related to servicing the debt.

ADSCR = CADS in a particular time period/Debt service requirement in that period

The debt service requirement in a particular period is equal to the sum of principal repayments and finance charges which include interest and fees. ADSCR of 1.5 is considered to be normally acceptable. If the lenders perceived the project to be risky, then will ask for higher ADSCR values, on the other hand, in case of project with very low degree of risk exposure, lenders will be willing to finance projects with DSCR value close to unity, when there is certainty that project will generate enough cash flows to service debt. Lenders requirement for the minimum value of ADSCR also varies between projects of various sectors. For instance, the minimum ADSCR for power projects or process plant project with off-take contract will be around 1.3. On the other hand, the minimum ADSCR requirement for merchant power plant with no off-take contract will be around 2.0. Lenders look at the ADSCR for each time period throughout the term of the loan and check that this does not fall below their required minimum at any time.