Comparison of alternatives by annual worth method:

In this method, the mutually exclusive alternatives are compared on the basis of equivalent uniform annual worth. The equivalent uniform annual worth represents the annual equivalent value of all the cash inflows and cash outflows of the alternatives at the given rate of interest per interest period. In this method of comparison, the equivalent uniform annual worth of all expenditures and incomes of the alternatives are determined using different compound interest factors namely capital recovery factor, sinking fund factor and annual worth factors for arithmetic and geometric gradient series etc. Since equivalent uniform annual worth of the alternatives over the useful life are determined, same procedure is followed irrespective of the life spans of the alternatives i.e. whether it is the comparison of equal life span alternatives or that of different life span alternatives. In other words, in case of comparison of different life span alternatives by annual worth method, the comparison is not made over the least common multiple of the life spans as is done in case of present worth and future worth method. The reason is that even if the comparison is made over the least common multiple of years, the equivalent uniform annual worth of the alternative for more than one cycle of cash flow will be exactly same as that of the first cycle provided the cash flow i.e. the costs and incomes of the alternative in the successive cycles is exactly same as that in the first cycle. Thus the comparison is made only for one cycle of cash flow of the alternatives. This serves as one of greater advantages of using this method over other methods of comparison of alternatives. However if the cash flows of the alternatives in the successive cycles are not the same as that in the first cycle, then a study period is selected and then the equivalent uniform annual worth of the cash flows of the alternatives are computed over the study period.

Now the comparison of mutually exclusive alternatives by annual worth method will be illustrated in the following examples. First the data presented in Example-2 will be used for comparison of the alternatives by the annual worth method.

Example -10 (Using data of Example-2)

There are two alternatives for purchasing a concrete mixer and following are the cash flow details;

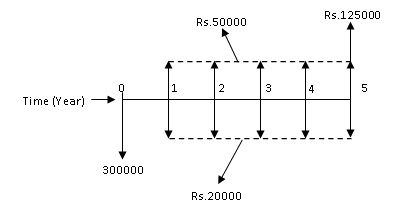

Alternative-1: Initial purchase cost = Rs.300000, Annual operating and maintenance cost = Rs.20000, Expected salvage value = Rs.125000, Useful life = 5 years.

Alternative-2: Initial purchase cost = Rs.200000, Annual operating and maintenance cost = Rs.35000, Expected salvage value = Rs.70000, Useful life = 5 years.

The annual revenue to be generated from production of concrete (by concrete mixer) from Alternative-1 and Alternative-2 are Rs.50000 and Rs.45000 respectively. Compute the equivalent uniform annual worth of the alternatives at the interest rate of 10% per year and find out the economical alternative.

Solution:

The cash flow diagram of Alternative-1 i.e. Fig. 2.3 is shown here again for ready reference.

Fig. 2.3 Cash flow diagram of Alternative -1

The equivalent uniform annual worth of Alternative-1 i.e. AW1 is computed as follows;

![]()

![]()

Here Rs.20000 and Rs.50000 are annual amounts.

Now putting the values of different compound interest factors;

![]()

![]()

AW1= - Rs.28665