Example -20

The cash flow details of a public project is as follows

Initial cost = Rs.21000000

Annual operating cost = Rs.1600000

Worth of annual benefits = Rs.5000000

Worth of annual disbenefits = Rs.1100000

Salvage value = Rs.4000000

Interest rate per year = 8% and useful lie = 30 Years

Using benefit-cost ratio method (both conventional and modified), find out the economical acceptability of the public project. Use PW, AW and FW methods to find out the equivalent worth of costs, benefits and disbenefits.

Solution:

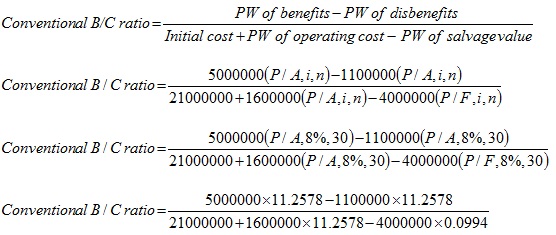

First the conventional benefit-cost ratio (B/C ratio) of the project is computed.

Conventional B/C ratio using Present worth:

The conventional benefit-cost ratio of the public project is calculated as follows;

Conventional B/C ratio = 1.137

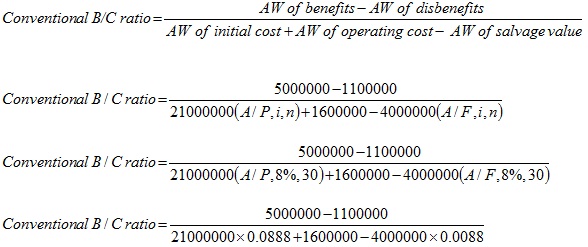

Conventional B/C ratio using Annual worth:

Conventional B/C ratio = 1.137

Conventional B/C ratio = 1.137

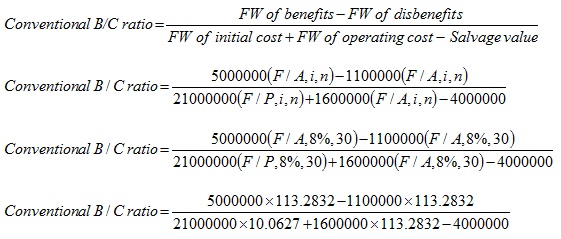

Conventional B/C ratio using Future worth:

Conventional B/C ratio = 1.137

As calculated above, the conventional benefit-cost ratio is found to be same by using any of the equivalent worth methods i.e. PW method, AW method or FW method. As the benefit-cost ratio of the public project is 1.137 (i.e. greater than 1.0), the project is acceptable.

Now the modified benefit-cost ratio (B/C ratio) of the project is calculated.