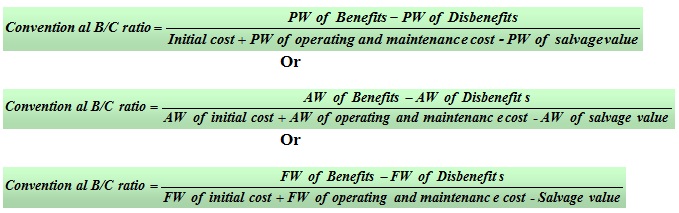

Conventional B/C ratio

The conventional benefit-cost ratio of a project is mentioned as follows;

The disbenefits associated with the project are subtracted from the benefits in the numerator of the ratio to obtain the net benefit associated with the project. Similarly the equivalent worth of salvage value of the initial investment is subtracted from equivalent worth of cost in the denominator of the ratio. The total cost mainly consists of initial cost (initial capital investment) plus the operating and maintenance cost.

As already stated the equivalent worth may be calculated either by present worth method, annual worth method or future worth method. Thus the expression for conventional benefit-cost ratio (B/C ratio) is mentioned as follows;

In the above expressions, PW, AW, and FW refer to equivalent present worth, annual worth and future worth respectively.

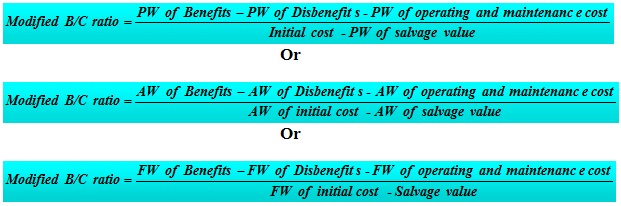

Modified B/C ratio

In the modified benefit-cost ratio method, the operating and maintenance cost is subtracted from the benefits in the numerator of the ratio. In other words, operating and maintenance cost is considered similar to the disbenefits. The expression for modified benefit-cost ratio using PW, AW or FW is given as follows;

A project is considered to be acceptable when the conventional or modified B/C ratio is greater than or equal to 1.0. The illustration of conventional and modified B/C ratio methods is described in the following example.