Contents

Properties of the system

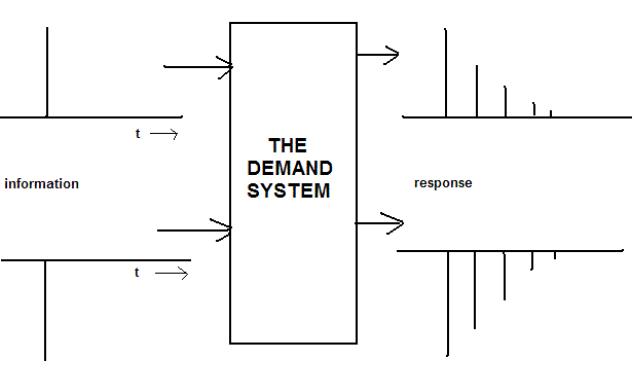

Keeping the above factors in mind we form the following system:The

input to our system is the information we get everyday related to the

company, and the output is the change in demand .

We assume the system to be a discrete time system wherein we take

into account the demand change at the end of the day.We can think of this system in terms of a very simple model which

takes it's input as a positive spike or impulse, for a piece of information

which is beneficial

to the company performance, and the output is increase in demand for

the stock which persists for several days though reducing in magnitude.

Similarly a bad news can be represented as a negative impulse , and

the output will be decrease in demand whose magnitude will go on

eroding with time.

Though it cannot be quantified , we take an abstract assumption

that the magnitude of the impulse represents the extent to which the

information is beneficial or detrimental to the company'sp rospects.

Now, we analyse our system on the basis of the properties that it may

possess:

1)

Memory : The system has memory. This is evident from the impulse

response of the system which demonstrates that an information has a

persisting effect on the demand for a stock. For example If a company

comes out with good quarterly results , the stock is likely to remain in

high demand for some time.

2) Causality : The system we are considering is noncausal.

Investors are

constantly watching macroeconomic variables to try and determine

when the next downturn in the economy will happen. Investors are

often right when they predict the future growth rate of the economy. As

a result, they often sell off their shares before the economy goes into a

decline making it look like the stock market is causing a recession. In

reality the causality runs the other way because the two things that

causes price to change are changes in supply or changes in demand. An

interesting observation can be made here that a system based just

upon the company's performance as inputs would be causal , it is

human analysis and the presence of information that make it noncausal.

3) Stability : The system is stable, there exists a balance in the market due

to the presence of bulls and bears. An upward march in prices is

checked by the presence of bears who earn money on falling stocks,

while the bulls ensure that stocks don't plummet to abysmal values.

4) Shiftinvariance:

We cannot really comment whether the system is

shiftinvariant,

this is because the system itself is variable with time, for

example the number of the buyers and sellers might change , the initial

price of the stock might be different and so on.

On the premise that the system does not vary with time, if we consider

one input signal at a time keeping others fixed, we find that the system

still remains shiftvariant.

5) Linearity: Considering the magnitude of the two informations received

to be the same, the change in price would be double the individual

change that would have otherwise occurred. This is if we assume the

buyers to have an infinite purchasing power, and hence the prices can

go on increasing indefinitely without any constraint on the buyer. Also

the influence of the bulls and the bears is neglected. But since these

assumptions are not justified in the real scenario, the system is not

linear. But we can see that the market exhibits liearity in a certain range

of prices.

6) Invertibility: Since the system maps more than one input signal to an

output signal, we cannot comment upon its invertibility.

Now, let us return to the basic system that we were considering.

This system has as its inputs the time varying signals of supply and

demand and the output is the price at the end of the day. Also, the system

works with discretetime

signals.

We observe that since the supply is constant the %change in price

curve follows the %change in demand curve.

Hence the system properties:

1)

Memory :The

system has no memory, as the price is solely

determined by the demand at that particular instance of time.

2) Causality:The

system is causal, since it possesses no memory.

3) Shiftinvariance: The system is shiftvariant,

as the change in price is

dependent upon the original price of the stock. For example if a stock is

already overpriced the same demand would cause less change in price

than it would cause to an undervalued

stock.

4) Stability: The system is stable, since bounded change in demand will

always result in bounded change in price of the stock.

5) Linearity: The system is linear within a price range but practically due

to limited purchasing power and the effect of bulls and bears it is non

linear.

6) Invertibility: The system is not invertible since one value of change in

demand can produce different changes in price depending upon the

original price.

Thus, we conclude that although the practical model for the stock market

is fairly complicated, we can get a good idea of how it functions by

making a few simplifying assumptions and looking at it from the signals

and systems point of view.

Use Of Application In Real Life

Since we are dealing with a real life application i.e the stock market, the theory we've proposed can be used to study the stock market in a simpler manner.Acknowledgement

We would like to thank Prof. V.M .Gadre for his invaluable guidance.