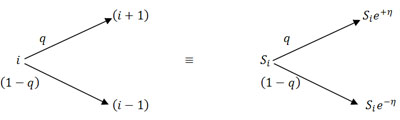

In case someone is interested to understand this concept using the basic idea of transition, then we have the following equivalent diagram (Figure 16) which would make things clear for the reader.

Figure: 10.6: Equivalent concept of price movement for a stock considering binomial tree

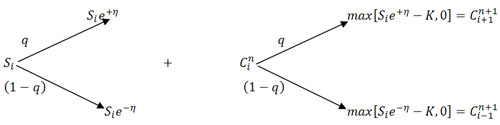

Let  =Value of a claim at time =Value of a claim at time  in state in state  , where as per the usual notation we have the call as the option to buy, while put is that which denotes the option to sell. , where as per the usual notation we have the call as the option to buy, while put is that which denotes the option to sell.

Consider the contract maturity case for the example (Figure 10.7) when we have the call option and for which  as per notation is the strike price. as per notation is the strike price.

Figure: 10.7: Concept of price movement for a stock as well as the option, where the portfolio consists of the stock and option

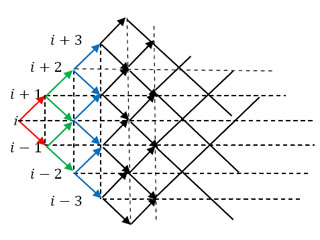

Figure: 10.8: Binomial tree concept extended for more than one stage and more than one state

|