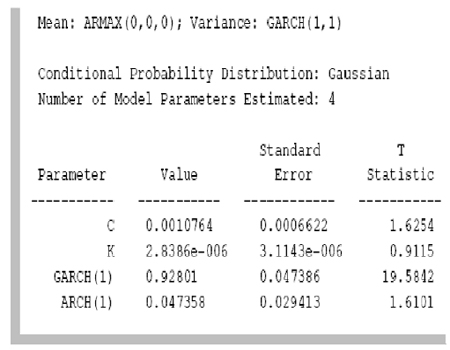

Now again going back to our example. We estimate the model parameters and then examine the estimated GARCH model (time series model), and the parameters are estimated and their standard errors obtained for BASF are shown in Figure.5.4:

Figure.5.4. Parameter estimates and their Standard Errors of the GARCH (1,1) model for BASF

Now, substituting these estimates in the definition of the GARCH (1,1) the constant conditional mean GARCH(1,1) conditional variance model that best fits the observed data is:

|