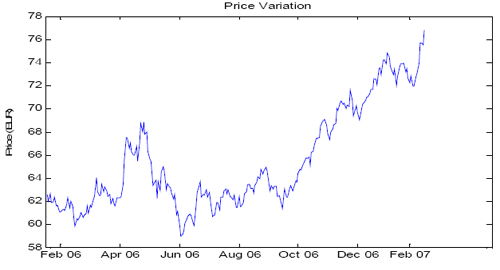

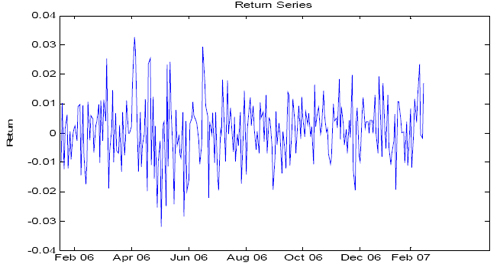

Example 5.5

Consider the financial time series which for case we take the example of BASF (a script in German stock exchange index DAX) prices from February 7, 2006 through February 6, 2007 and as required we first illustrate in Figure 5.2 and Figure 5.3 the prices and returns for this particular stock.

Figure 5.2: BASF prices from 7-Feb-2006 to 6-Feb-2007

Figure 5.3: BASF return series from 7-Feb-2006 to 6-Feb-2007

One already knows that a very simple concept to check the stationarity of a stochastic process is by considering either the first or second difference of the stochastic cprocess.

|