INTEREST RATE RISK

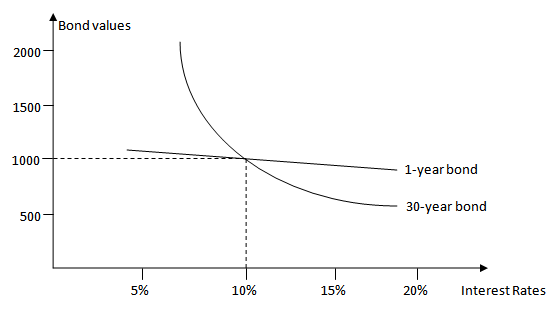

The fluctuations in the interest rate have an important impact on the value of bond. The risk that bond holders face from fluctuating interest rate is called interest rate risk. How much risk the bond has from interest rate fluctuation depends on the sensitivity of the price to interest rate changes. The sensitivity directly depends on two things: time to maturity, and the coupon rate. The longer the time to maturity, the greater will be the interest rate risk. And, lower the coupon rate, greater will be the interest rate risk. The following figure shows the variation between the bond values and the interest rates for two bonds with 10% coupon rate for different time to maturity (one with 1 year to maturity and another one with 30 years to maturity).

Figure: 2 Variation of the Value of Bonds with 10% Coupon Rate for Different Interest Rates

The slope of the line connecting the prices is much steeper for the bond with 30 year maturity than for the bond with 1 year maturity. For bond with longer maturity, a relatively small change in interest rate could lead to a substantial change in the bond's value. On the other hand, the price of 1 year bond is relatively insensitive to interest rate change. The reason why the longer-term bonds have greater interest rate sensitivity is that a large portion of the bond's value comes from the face value amount. The present value of this amount will not affected by a small change in interest rates if it is to be received in one year. On the other hand, if the face value amount is to be received after 30 years, even a small change in the interest rate can have a significant effect once it is compounded for 30 years. The present value of this face value amount becomes more volatile with a longer-term bond as a result.