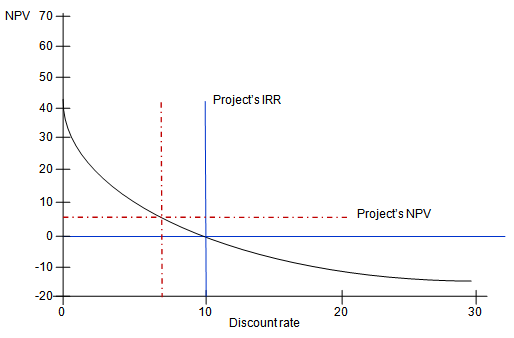

NPV and IRR are interrelated. The relationship of NPV with IRR could be shown using an NPV profile, where NPV is shown as a function of discount rate. The NPV profile shows the value of the project at different discount rates. It can be seen that if the project's NPV is greater than zero, then the project's IRR is greater than the project's cost of capital.

Figure: 1 NPV Profile of a Project

The two methods will yield the same result for projects which are both independent and conventional. Independent projects are those project where undertaking that project will not prevent investing in another project. And, conventional projects are those projects with initial cash flow followed by subsequent expected future cash flows, which are expected to be positive.

However, NPV and IRR yield different results in case of mutually exclusive projects. A project is considered to be a mutually exclusive if the selection of the project results in exclusion of other projects. In case of mutually exclusive projects, the IRR and NPV will give conflicting recommendations because of the difference in (i) size of the project; and (ii) cash flow timing. Amongst the mutually exclusive projects, if one of the projects is a project of smaller value, then that project will have higher IRR but smaller NPV. In such conflicting situation, the decision rule should be to select project that will add the most wealth, i.e. the project with higher NPV. On the other hand, due to the differences in cash flow timings, if the NPV and IRR values for the mutually exclusive projects are such that there is conflict in the choice of the project then also decision rule based on NPV should be superior to IRR decision rule. For instance, if A and B are two mutually projects and NPV and IRR for the two projects are 85.08 and 18.08% for project A and 93.07 and 17.34% for project B, then decision rule should still be based on NPV, Project B should be preferred project.