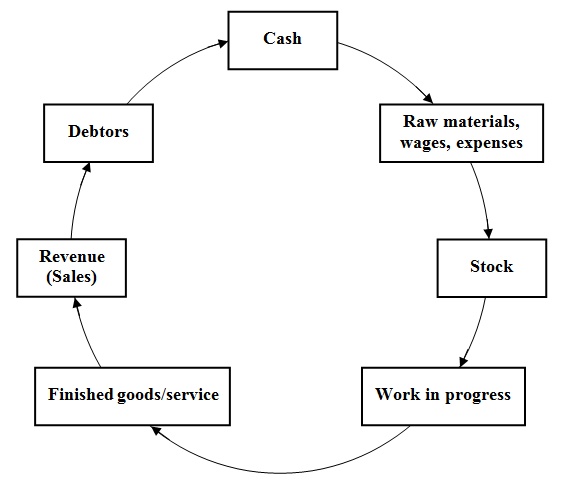

Working capital is represented in a continuous cycle known as operating cycle and a typical operating cycle is shown in Fig. 6.1. The operating cycle is also referred to as working capital cycle or current assets and current liabilities cycle. The operating cycle starts with acquiring raw materials and consumables using cash (or on credit), maintaining their inventory, use in production, obtaining finished goods (or service) followed by sales, receipt of payment against the bill and finally realizing the cash, which completes the operating cycle and the same process is again continued. In other words in the operating cycle, there is continuous flow from cash to suppliers, to inventory, to finished goods (or service), to accounts receivable and then to cash again. The length of an operating cycle (i.e. duration) depends on the number of stages involved (as mentioned above) and the average length (i.e. duration) of each stage. For a construction company undertaking a project, the operating cycle begins with procurement of construction materials and other consumables with cash (either available or from advance if any received from the owner of the project) or on credit from the suppliers. The quantities of these items to be purchased depend on how much to be used during a given period of time and how much to be kept in stock. Further cash is used for payment of wages to labourers employed in the project and payment of equipment rental charges to the equipment renting firm along with the payment of overhead expenses. If the equipment is owned by the construction company, then cash is utilized for meting the operating cost of the equipment employed in the project. The construction material suppliers and equipment renting firm are regarded as creditors if the company acquires these items on credit. After completion of a portion of work, the construction company raises the bill against the activities carried out during that period of time i.e. billing period which may be one month or two months (i.e. as per conditions of contract between the owner and the construction company). The billed amount becomes accounts receivable and owner of the project is regarded as debtor to the construction company till the receipt of payment against the bill. The receipt of payment against the bill and realization of cash completes the operating cycle and the process continues. The construction company must have sufficient working capital to meet expenses of materials, equipment, labour and overhead till the receipt of payment from the client (i.e. owner of the project). The estimation of working capital requirement is an important aspect of working capital management. The factors those affect the working capital requirement are nature and size of the business, type of raw materials, production process, credit policy, duration of operating cycle, volume of production and sales etc.

Fig. 6.1 Operating cycle