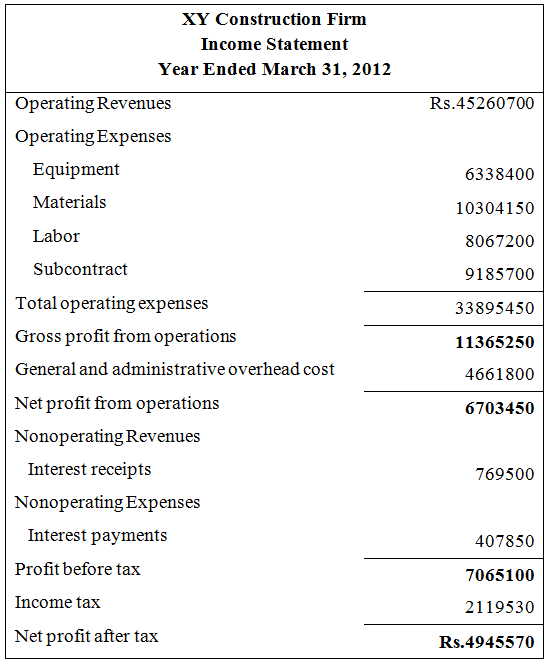

In the income statement, the operating revenues and expenses are shown first. From these records, the gross profit from operations is calculated. After that the net profit from operations is calculated by the subtracting the overhead cost from the gross profit (from operations). The nonoperating revenue and expenses are then recorded. The profit before tax is then equal to net profit from operations less the nonoperating revenue and expenses. It may be noted here that the nonoperating revenue is added whereas nonoperating expense is subtracted from net profit from operations. After that the net profit after tax is calculated by subtracting the income tax (at an appropriate income tax rate) from profit before tax.

A typical income statement of a construction firm is shown as follows.

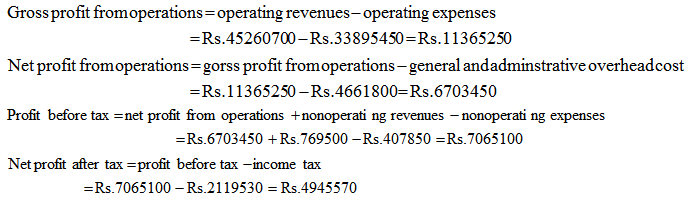

For the above income statement, the calculations of gross profit from operations, net profit from operations, profit before tax and net profit after tax are presented below.