The capitalized cost of the annual operating cost can also be calculated by considering Rs.800000 from end of year 1 till end of year 10 and Rs.900000 from end of year 11 till infinity. The calculation is shown below.

![]()

In this expression, first the present worth of uniform series with annual amount of Rs.800000 for first 10 years is calculated. Then the capitalized cost of Rs.900000 from end of year 11 till infinity is calculated in the same manner as for Rs.100000 in the first approach.

Capitalized cost = -Rs.10579080

Thus it can be seen that the capitalized cost of annual operating cost by both ways is same. The minor difference between the values is due to the effect of decimal points in the calculations.

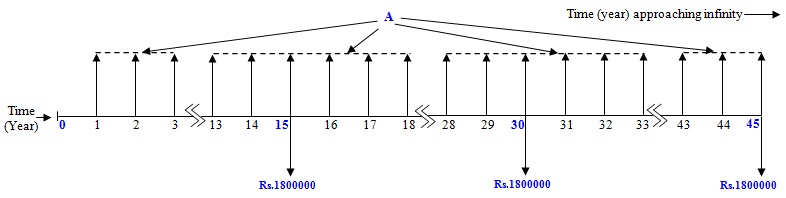

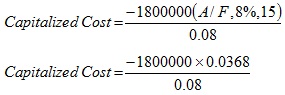

Capitalized cost of renovation component:

The renovation will take place at the end of every 15 years i.e. at the end of 15th year, 30th year, 45th year etc. In order to calculate the capitalized cost of renovation component (Rs.1800000) at the end of every 15 years, first the uniform annual amount ‘A’ of the equivalent uniform series for the first 15 years is calculated. This amount ‘A’ will be same for the subsequent intervals i.e. from end of year 16 till end of year 30, from end of year 31 till end of till year 45 and so on (shown in Fig. 2.31). Then the uniform amount ‘A’ is divided by the interest rate.

Fig. 2.31 Cash flow diagram for periodic renovation cost of the project

Capitalized cost = -Rs.828000

Now the total capitalized cost of the project is equal to initial cost plus capitalized cost of annual operating cost and renovation cost.

Capitalized cost = -Rs.15000000 -Rs.10579000 -Rs.828000

Capitalized cost = -Rs.26407000

Therefore the capitalized cost of the infrastructure development project is Rs.26407000.