| |

Properties of Brownian Motion

One denotes the Brownian motion by  where in general where in general  , and the following properties hold: , and the following properties hold:

a.Given  , ,  , , ,…., ,….,  are mutually independent are mutually independent  and and  . Such a process has independent moments. . Such a process has independent moments.

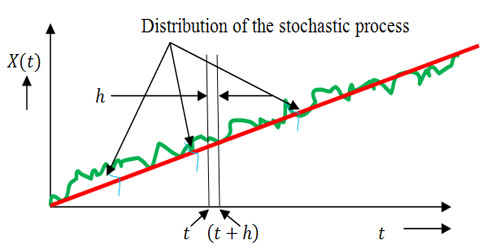

b.For any  , ,  , ,  depends only on depends only on  and not and not  . Which means the process has stationary increments, Figure 6.4. . Which means the process has stationary increments, Figure 6.4.

Figure 6.4: A hypothetical example of a stationary process with respect to variance

|